Divido

Improving checkout conversions for Divido’s white-labelled consumer finance platform

Role

Senior Product Designer

Industry

Fintech - Retail Finance

Year

2023 / 24

Overview

Divido, a UK-based fintech company, is revolutionising retail finance with its whitelabel embedded lending technology. Unlike competitors such as Klarna, Divido doesn't directly provide credit. Instead, it operates as a marketplace where lenders compete to provide the most suitable credit options. To address this dynamic market, Divido has developed a robust technology and product stack, facilitating lenders in offering retail finance solutions swiftly, and empowering merchants with a feasible path to providing finance across various markets.

In April 2023, I joined Divido as their first full-time product design hire. Initially, I joined the Merchant Squad to enhance their Merchant Platform offering with additional functionality. I swiftly transitioned into the role of Lead Product Designer, overseeing the entire product lifecycle of multiple offerings. Collaborating closely with product strategists, technical leads, engineering teams, and marketing, I facilitated the delivery of more scalable and flexible customer experiences.

Problem statement

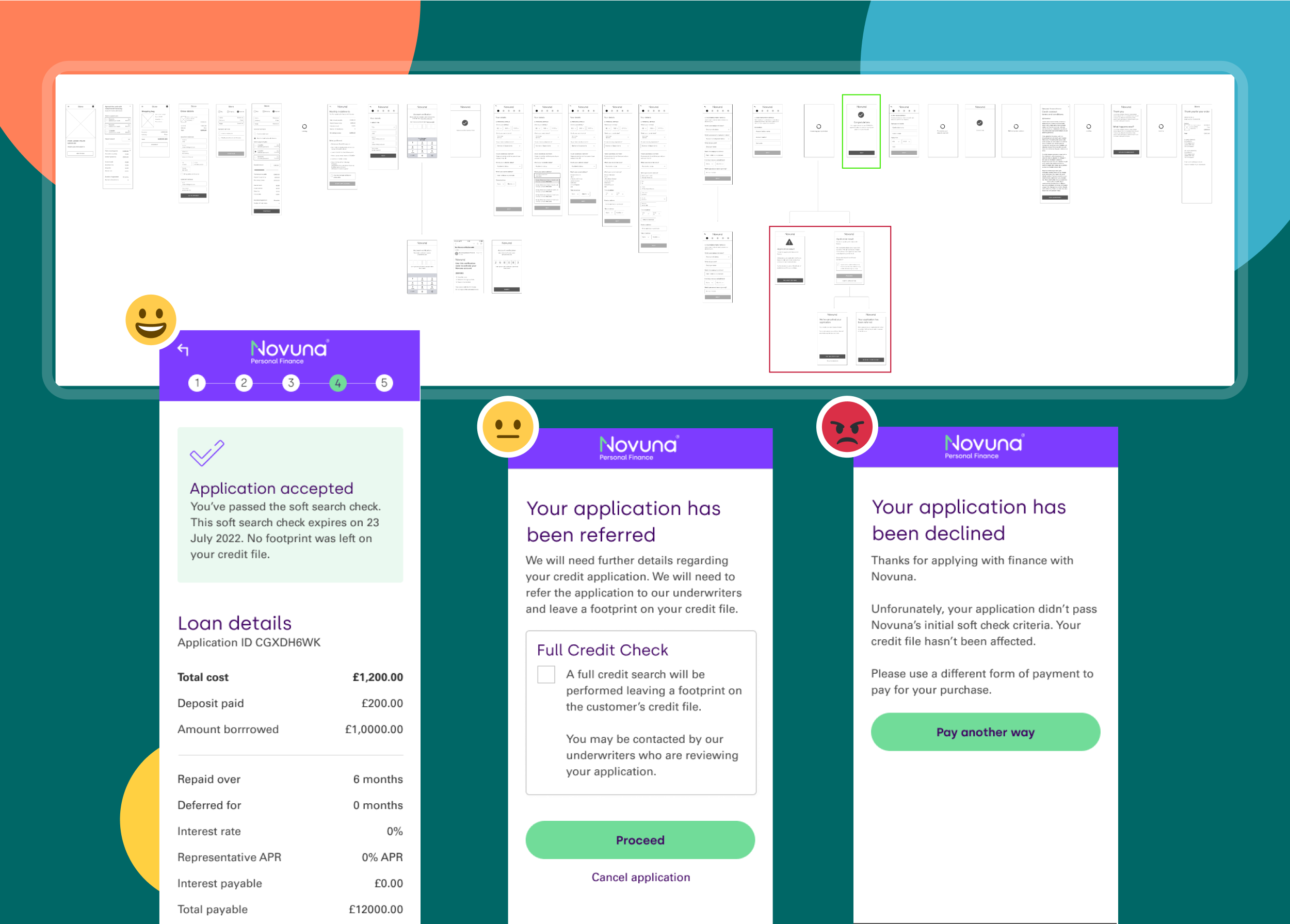

Divido’s white-labelled consumer finance platform enables shoppers to access retail finance at checkout. However, a key point of friction existed when customers were declined for finance based on their initial deposit and repayment term selections. With no ability to adjust their application or explore alternative offers, users were sent back to the checkout to choose a different payment method—often leading to frustration, drop-off, and lost revenue for merchants.

Challenges & objectives

Key business challenges:

- High cart abandonment rates triggered by finance application declines.

- Loss of customer trust and satisfaction due to lack of flexibility in the checkout journey.

- Reduced overall conversion rates for merchants using Divido’s finance products.

- Limited visibility for lenders to influence application outcomes post-decline.

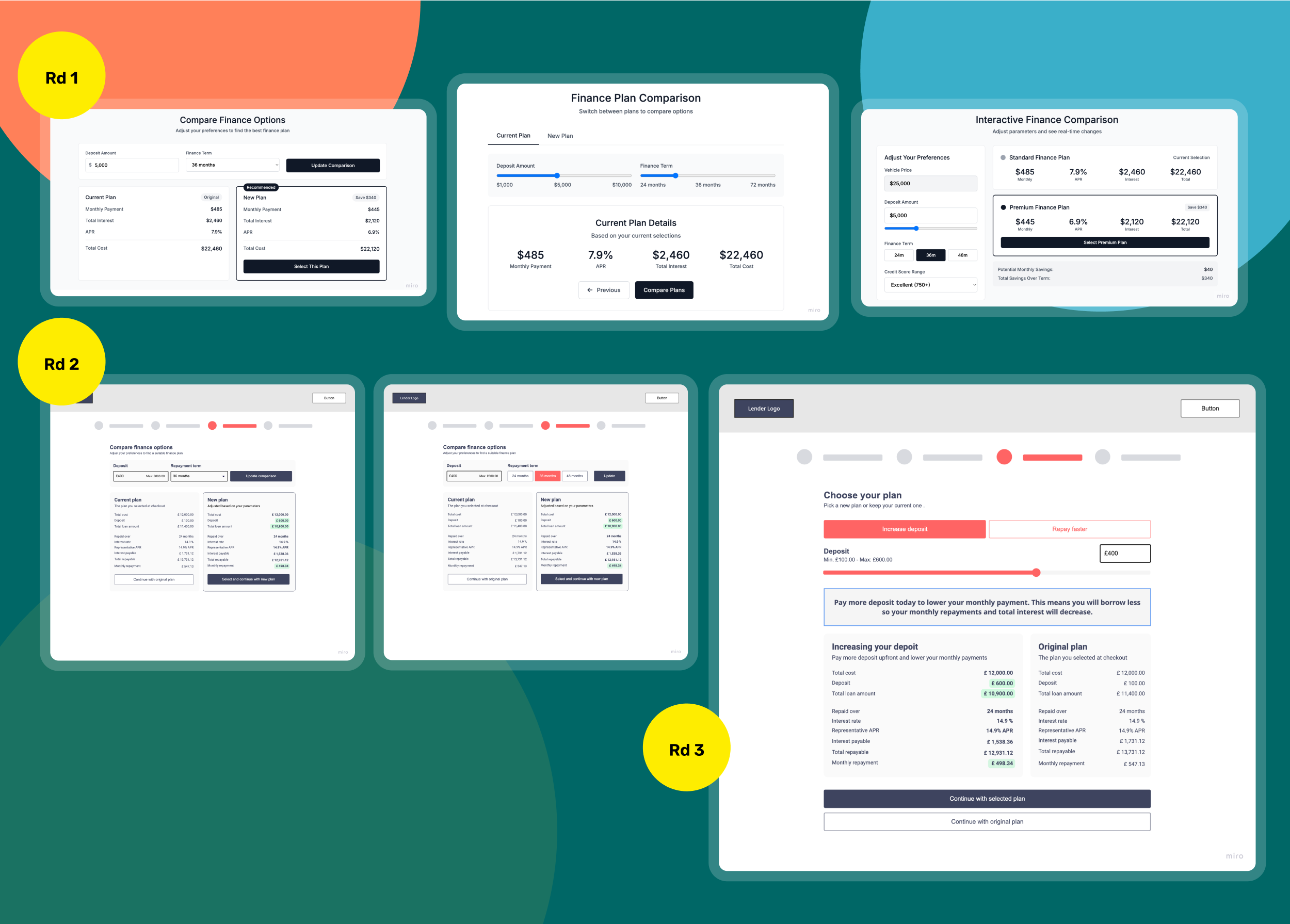

Approach

As the UX lead, I partnered with product, engineering, and commercial stakeholders to reimagine the post-decline experience. Our goal was to provide consumers with a dynamic, guided path to reshape their finance terms without abandoning the purchase flow.

We conducted:

- A review of historical application data to understand common decline reasons.

- Journey mapping and service blueprinting to identify intervention points.

- Wireframes and prototypes tested with real users to validate comprehension and usability.

- Collaboration with lenders to define offer criteria and guardrails for restructuring finance terms.

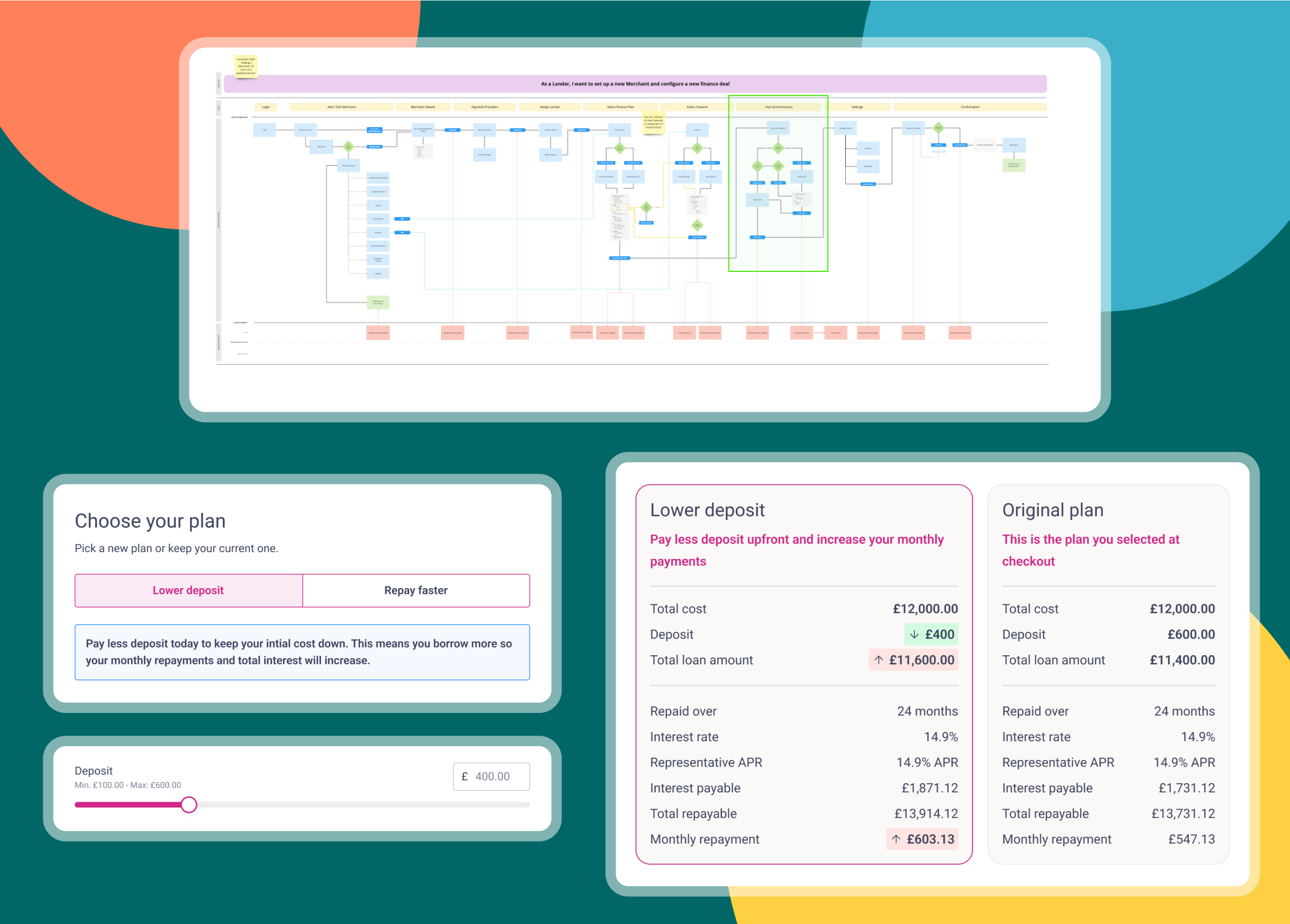

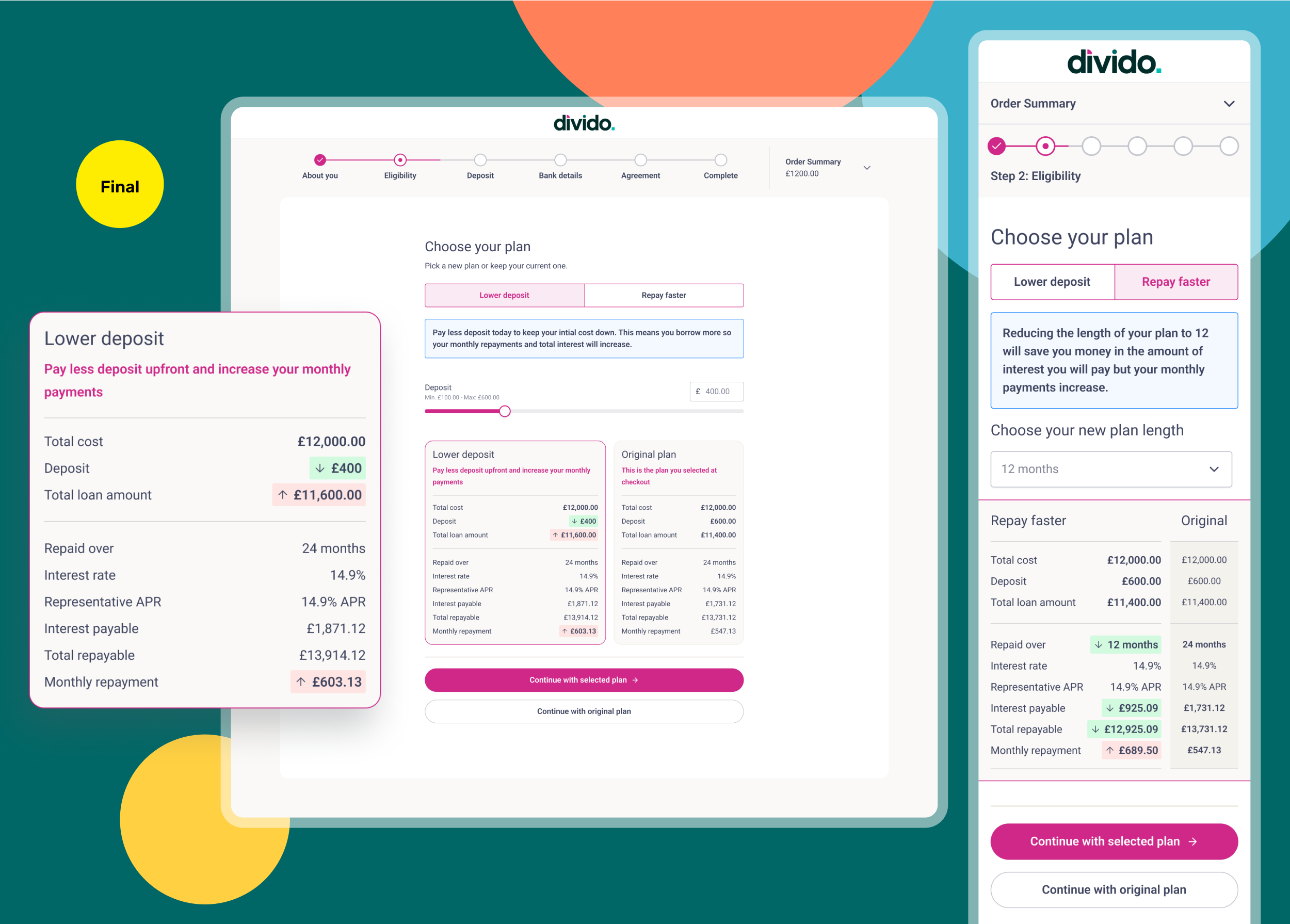

Solution

We introduced Finance Matcher, an adaptive feature within the application journey that activated when users were declined for their initial finance terms. Instead of being redirected away:

- Users were either presented with a lender-generated alternative (e.g. higher deposit, extended term) or…

- Given the ability to tailor their own terms within lender-approved parameters (e.g. minimum deposit %, max term length).

- Dynamic guidance and progress indicators helped users understand what changes could increase their chances of approval.

- Fully brandable UI elements ensured a seamless, on-brand experience for each merchant.

Results & impact

The launch of Finance Matcher had a significant and measurable impact on both user experience and commercial outcomes. By enabling consumers to adjust their finance terms dynamically rather than abandoning their purchase, we were able to reduce friction at a critical stage of the checkout journey. This not only improved customer satisfaction but also drove meaningful improvements in conversion metrics for merchants and engagement for lenders.

- Positive qualitative feedback from users highlighting “ease of adjustment” and a sense of “transparency and control.”

- Strengthened merchant confidence in Divido’s platform, with several clients citing the feature as a competitive differentiator.

- Enhanced lender participation by allowing their preferred fallback terms to be integrated directly into the consumer journey.

67% uplift

in finance application completions following initial decline.

82% reduction

in cart abandonment at the point of finance decline.

Closing summary

Finance Matcher successfully addressed a key pain point in the consumer finance application journey — transforming a previously frustrating end-point into a dynamic opportunity for recovery. By giving users more control and lenders more flexibility, we improved outcomes across the board: increased conversions, reduced drop-offs, and elevated the overall experience for all stakeholders. The project was a great example of collaborative, insight-led design delivering tangible business value.

Lessons learnt

Early engagement with lenders and helps shape more effective product constraints and opportunities.

Giving users clear, guided pathways — rather than open-ended options — significantly improves decision confidence.

We proved that even small, smart UX tweaks in the right place can drive large business results.

What I'd do differently

Integrate real-time eligibility feedback earlier in the flow to help set clearer expectations before the point of decline.

Push for deeper user testing with a broader demographic to validate edge cases and accessibility needs.

Begin customisation and branding design tracks earlier to better support multi-merchant rollout readiness.